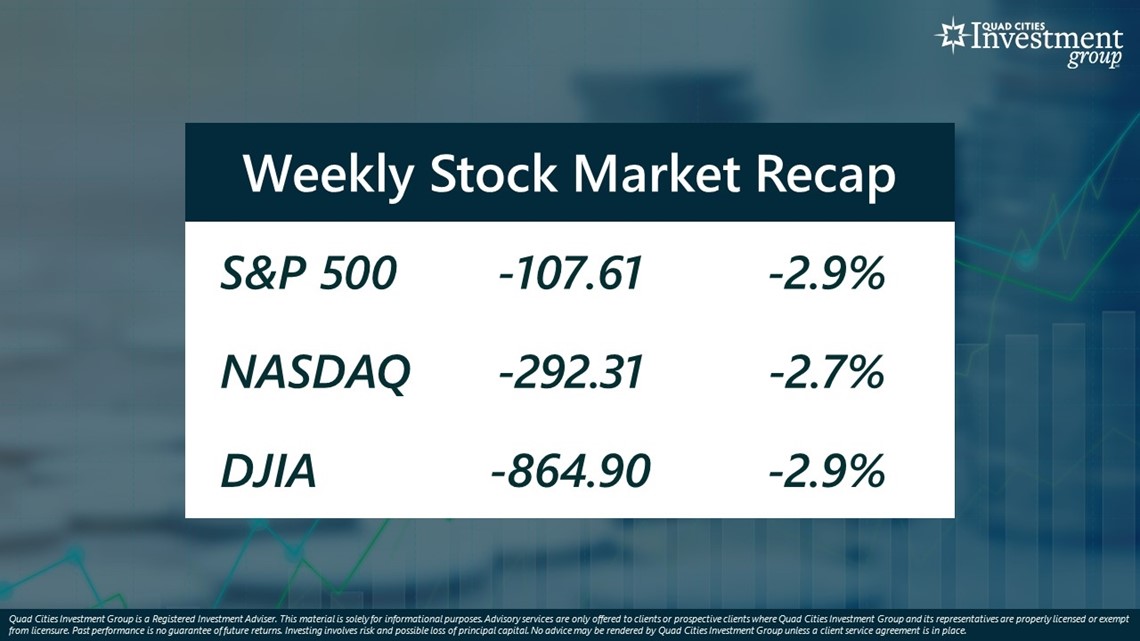

MOLINE, Ill. — Over the last week, the benchmark S&P 500 stock index fell by 2.9%, NASDAQ fell by 2.7% and DJIA fell by 2.9%.

In Hurricane Ian's wake, Mark Grywacheski of the Quad Cities Investment Group joined WQAD's David Bohlman on Monday morning to discuss how Quad Citizens can best financially prepare for a natural disaster.

Here's the full conversation:

David: Here in the Midwest, we often have to deal with the aftermath of tornados or flooding. What’s your advice on how to best financially prepare for some type of natural disaster?

Mark: At a minimum, set aside enough money to cover 3-6 months of living expenses. But one of the biggest factors to consider is if you should set aside even more (6-12 months of living expenses) is your ability to return to work once the initial disaster is over. Because what we’re seeing in Florida is that many people can’t return to work because that workplace building is simply gone. Now, today more than ever, people can/do work remotely- you can still receive a paycheck. But for many, if that workplace building is destroyed, they could be out of work for 6-12 months. And you need to consider that not only will you have day-to-day living expenses, but also those large cash outflows to rebuild your home and provide for your family. If you do lose your job, certainly unemployment insurance does help, but it likely won’t be enough to replace your full paycheck.

David: How should people go about building their emergency fund?

Mark: The first step is to create a budget that lists your cash income and monthly expenses. This allows you to identify what costs are necessary living expenses (food/clothing/housing/insurance) vs non-essential costs like entertainment. And it’s those necessary living expenses for which you need to build this emergency fund. Every month/paycheck set aside some money, or dedicate your annual tax refund, to the emergency fund. But as you’re building this emergency reserve of money, it takes a level of discipline to not use that money- it’s just for an emergency.

David: How should these emergency funds be invested? Should people just put their money in a savings account or can they put it in the stock market and try to get a higher return?

Mark: The focus should be on safe, low-risk, easy-to-access investments. You want the money there when you need it. I’d avoid the stock market or anything where the value can fluctuate. For example, as we’ve seen this past year in the stock market, you don’t want to have $20K set aside in stocks but when you need to use it the value is now down to $16K. Same with CDs- many have early withdrawal restrictions/penalties. I’d suggest using a savings account, or even better, an M/M account. Many M/M accounts are now offering a 2.25% yield.

David: We’re hearing more and more reports that Hurricane Ian has been impacting low-income families the most. Why are we seeing that and is that to be expected for most natural disasters?

Mark: Historically, low-income families and retirees have less ability to set money aside for some type of emergency fund. Most of their income is already being spent just to cover everyday basic necessities. But also, with this very high rate of inflation we have, we’ve already seen Americans being forced to pull money from their savings and retirement accounts just to cover the costs of these high consumer prices. And what we’re seeing in Florida, unfortunately, is that any household emergency cash reserves have already been spent.

Watch "Your Money with Mark" segments Mondays during the 6 a.m. hour of Good Morning Quad Cities or on News 8's YouTube channel.

Quad Cities Investment Group is a Registered Investment Adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Quad Cities Investment Group and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Quad Cities Investment Group unless a client service agreement is in place.